Distributed/compressed regression rocks

Author: James Brand

Date: 2025-08-24

TL;DR: This is a quick post about a relatively new pair of packages meant for fast, SQL-backed, regressions with fixed effects in R and Python.

I’ve only recently discovered the Python package duckreg (by

Apoorva Lal and coauthors) and the R port dbreg by Grant

McDermott, but I wanted to make a quick post about how amazingly fast

these packages are after being blown away while testing them. Before I

was as familiar with R, from the outside I thought that

fixest was unbeatably fast for linear regression with fixed

effects. Generally, fixest is definitely still king for

most applied work. However, the benchmarks I’ll show below suggest that

it can be beaten in at least one case (extremely large data), which has

gotten me excited about big regressions using SQL backends. I wanted to

share the excitement with this brief post. Full disclosure, I made a

modest PR to dbreg recently so this is probably partly self

promotion.

The idea(s) behind

duckreg/dbreg

These packages are supported by a couple of key papers:

- Wong et al. (2021)

- Demonstrates the optimal (lossless) “compression” that can be applied to large datasets to allow estimation of linear regressions and standard errors

- Wooldridge

(2021)

- Introduces the two-way Mundlak estimator, (among other things)

allowing the inclusion of unit- and time- effects without “absorbing”

the fixed effects in the ways common packages (e.g.,

fixestin R,reghdfein Stata,FixedEffectModelsin Julia) usually do.

- Introduces the two-way Mundlak estimator, (among other things)

allowing the inclusion of unit- and time- effects without “absorbing”

the fixed effects in the ways common packages (e.g.,

In short, these two papers together show that (a) regressions can be broken down into a “compression” step, which uses any desired backend to shrink large datasets into much smaller matrices, and then an incredibly fast estimation step using that output, and (b) that two-way fixed effect regressions can be estimated simply by including a couple of carefully constructed additional regressors. Combining these two means that we can run (up to) two-way fixed effect regressions by constructing the appropriate additional covariates and then compressing accordingly. Whether or not this is faster than existing methods when the data can fit in memory, the key value of this strategy is that it unlocks the ability to run regressions on datasets that are far too large to hold in memory. In testing these packages, I was able to run event study regressions with billions of observations and many millions of fixed effects, which had previously been infeasible, in just a couple of minutes.

Maybe the coolest thing about these ideas is that they’re basically

completely agnostic about the backend being used, becuase they rely on

simple group aggregations that can be done via SQL. So, barring the

implementation kinks of a young package, the tools dbreg

offers should be indifferent to whether you’re connecting to a DuckDB

database, a SQL Server endpoint, or just running a regression on a big

dataframe in memory. Switching between these seemlessly without jumping

between packages is, as someone who already alternates between

languages/tools too often for my taste, a very nice side benefit of the

use of generic SQL in both packages.

Benchmarking

The first pass at the dbreg package only implemented the

original Wong et. al (2021) approach to compression, which works very

well when covariates are discrete and when there are many observations

per unique combination of fixed effects and covariates, but does not

work well with continuous variables. The most recent version, however,

implements some of the “Mundlak” functionality in duckreg,

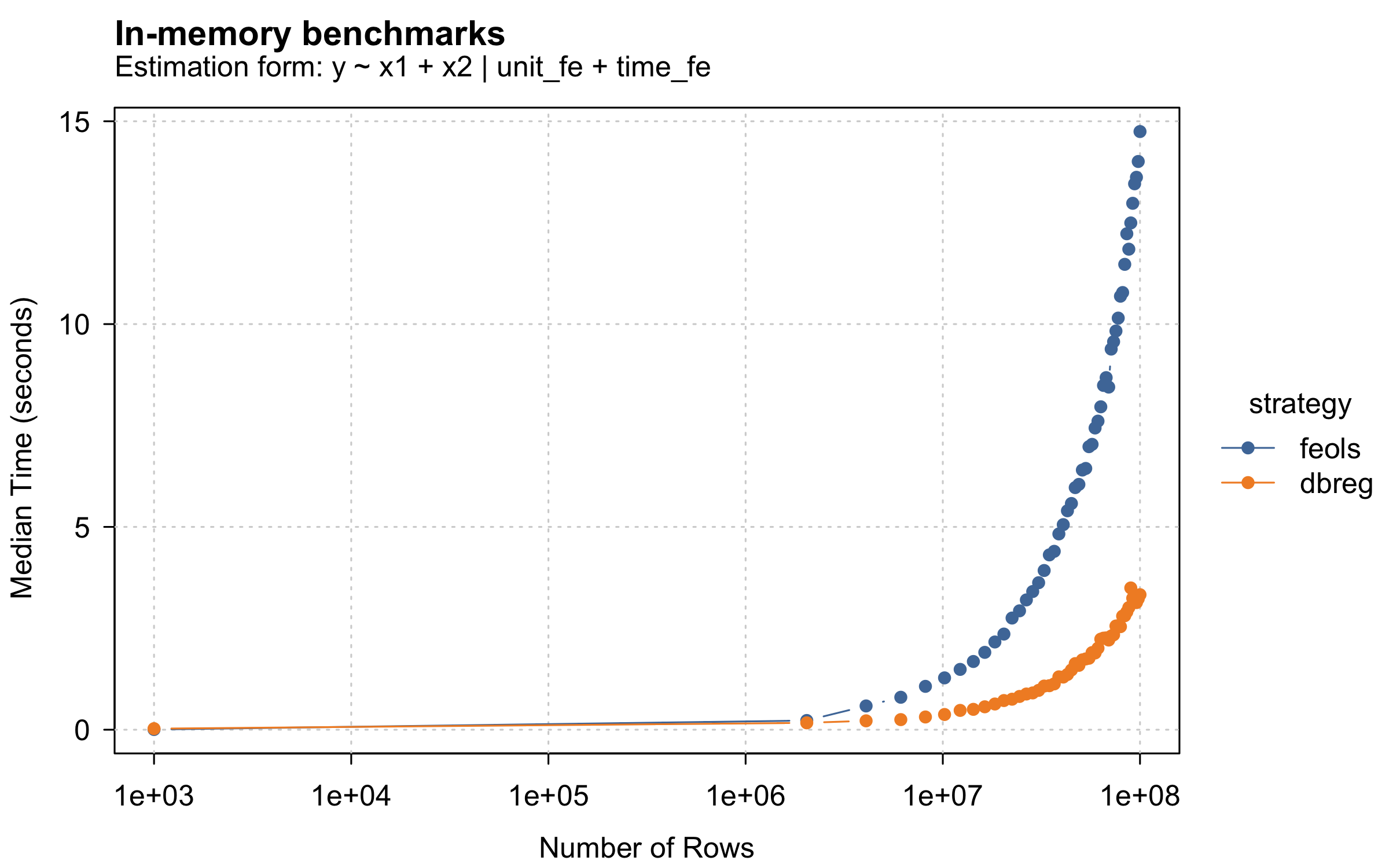

which has led to some amazing speed gains. As a benchmark, look at the

way fixest::feols and dbreg now scale with

sample size, in a setting with two covariates and two dimensions of

fixed effects (unit and time).

Clearly, dbreg beats feols handily here for

large datasets. For comparison, check out the

fixest/pyfixest benchmarks below (plot taken

from the latter’s repo). I didn’t spend any time trying to line up the

two benchmarks (i.e., the number and structure of fixed effects), but

you can see that in the two-FE case below (middle), feols

takes a little over a second here (~2.2 seconds) for the largest dataset

and is (barely) the fastest among all options. pyfixest is

also super fast, especially for larger regressions. However, for

regressions of comparable size (1e7 rows), dbreg takes less

than 0.4 seconds. Moreover, dbreg can handle 1e8 rows in

only 3.3 seconds. Again, not apples to apples, but handling ~10x the

data with only a ~60% time cost is awesome regardless.

Note that the speed here might seem like splitting hairs, but every little optimization matters at scale and in production settings. At tech companies with huge telemetry databases that far exceed the timings here, or in settings where inference is conducted via boostrapping the same regression repeatedly (both of which are common), we’re talking about a huge amount of time saved in practice.

Planned work

My experience has been that truely “big” data is stored in some sort

of database backend, and I’ve seen people sacrifice statistical power by

either sampling from these large datasets or using other statistical

methods that don’t make as good a use of the available data as

regression does. So, in a sense, duckreg and

dbreg were an overdue addition to the data scientist’s

toolkit that allow us to get lossless regressions on the “big data”

everyone has been talking about for decades. This alone has felt like

unlocking a superpower, and now the question is just how much of a DS’s

compute for other, or more complex, tasks can be offloaded to a SQL

endpoint, which is still unclear to me.

That said, I don’t expect dbreg to compete with

fixest for general use cases. However, I’m hoping to

continue contributing to dbreg, and I think there’s a good

bit more that can be done relatively quickly. Some low hanging fruit,

just to get it up to par with duckreg, are GLM support and

easy event study regressions, which likely cover a big share of common

use cases for regression on giant databases. Longer term, I’m fairly

bullish on more complex tasks like higher-order fixed effects or binned

scatters, and on speed optimizations for wider regressions than those

benchmarked here.